It’s tough to undertaking asset costs over a three-month horizon at the most effective of instances, by no means thoughts throughout a pivotal election in one among Europe’s largest economies and through a time when the Fed is more likely to put together for its first charge minimize later this 12 months. Nonetheless, this forecast endeavours to offer probably the most pertinent components to contemplate for the euro in Q3 with a sign of great FX ranges to bear in mind all through.

French Snap Election: A Trigger for Concern for Bond Market Buyers

After a heavy defeat within the European elections, French President Emmanuel Macron introduced a snap parliamentary election catching everybody off guard. Macron and his celebration have suffered a lack of assist most notably for the reason that pension reform protests and hasn’t fairly managed to get well because the right-wing opposition, the Nationwide Rally (RN), and a consortium of left leaning events appeared to fill the void.

Buyers don’t like uncertainty and a possible victory for RN might result in standoffs in the case of passing laws as conflicts between the president and a RN majority in parliament might frustrate processes.

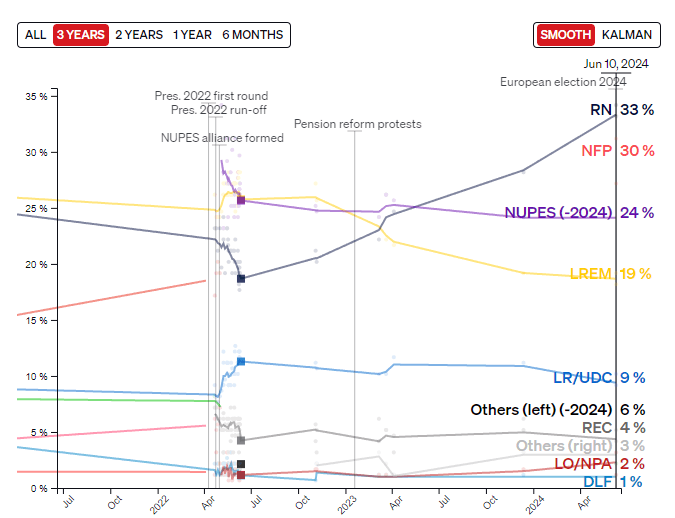

Evolution of Voter Preferences over the Final Three Years

Supply: Politico, ready by Richard Snow

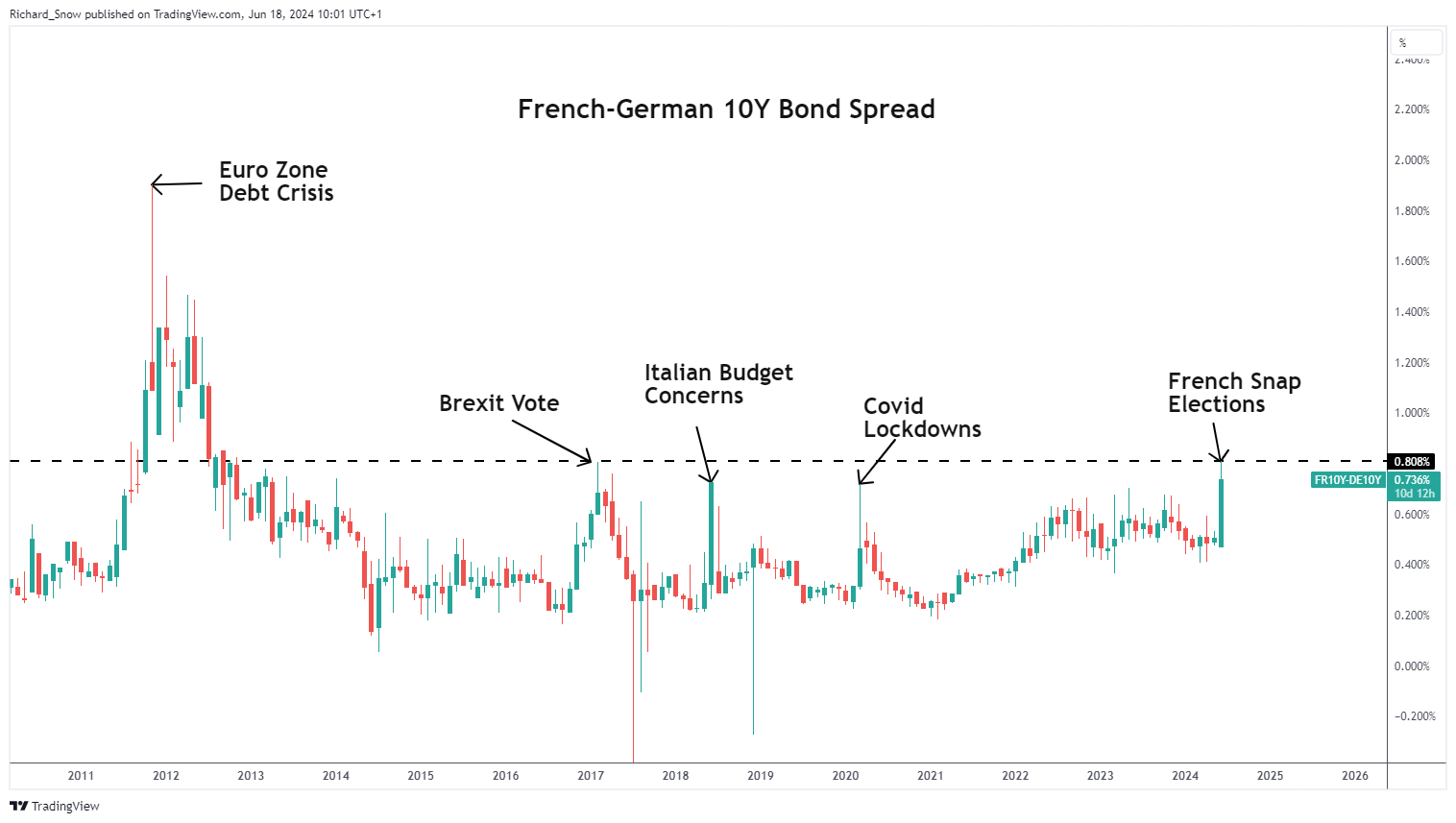

OAT-Bund spreads have widened to acquainted ranges, underscoring the affect of a possible political headache. RN have been recognized to be essential of the European Fee and will push in opposition to insurance policies handed down from Brussels, particularly the problem of deficit spending – one thing that issues the bond market given France already breaches EU tips of 60% debt to GDP ratio with its close to 110% determine. If first spherical elections on June thirtieth reveal something near the successful margin on the European election, then the French threat premium is more likely to rise additional and historical past warns us that the euro tends to sell-off when debt-laden international locations face greater borrowing prices. Contagion threat amongst periphery nations shall be chief amongst investor issues if the political panorama is headed for change.

French-German 10Y Bond Unfold (Danger Premium)

Supply: TradingView, ready by Richard Snow

After buying an intensive understanding of the basics impacting the Euro in Q3, why not see what the technical setup suggests by downloading the complete Euro forecast for the third quarter?

Really useful by Richard Snow

Get Your Free EUR Forecast

Fed Coverage to Outweigh ECB Fee Influence

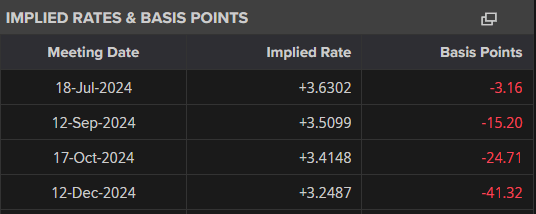

Whereas the ECB has already began to decrease rates of interest, anticipation across the Fed’s first minimize is more likely to be a significant driver of EUR/USD value motion in Q3. Market implied possibilities counsel the European Central Financial institution (ECB) is more likely to pause for the subsequent two conferences and reengage charge cuts in October and probably once more in December to chop a complete of 3 times in 2024. This lack of urgency, at a time when US information is pointing to a charge minimize later this 12 months, might maintain the euro supported within the absence of political instability in France.

Implied Charges and Foundation Factors

Supply: Refinitiv, ready by Richard Snow

For the US April and Might CPI information revealed disinflation is again on observe after months of cussed value pressures dented Fed officers’ confidence of a return to the two% goal. Financial development is moderating however the labour market stays strong. Ought to providers CPI and tremendous core inflation reveal significant declines, short-term US yields are more likely to see a sizeable drop, setting the scene for Fed officers to decrease charges earlier than November and probably minimize twice in 2024 regardless of June’s up to date dot plot which revealed just one minimize in 2024. The Fed refrains from coverage changes throughout US Presidential elections which suggests, if circumstances allow, the Fed might eye September extra severely and in doing so the greenback might lose additional floor to the euro.

The newest ECB forecasts counsel that inflation is simply more likely to return to 2% after 2025 and the governing council anticipates an uptick in inflation within the short-term – probably offering a tailwind for the euro in Q1.

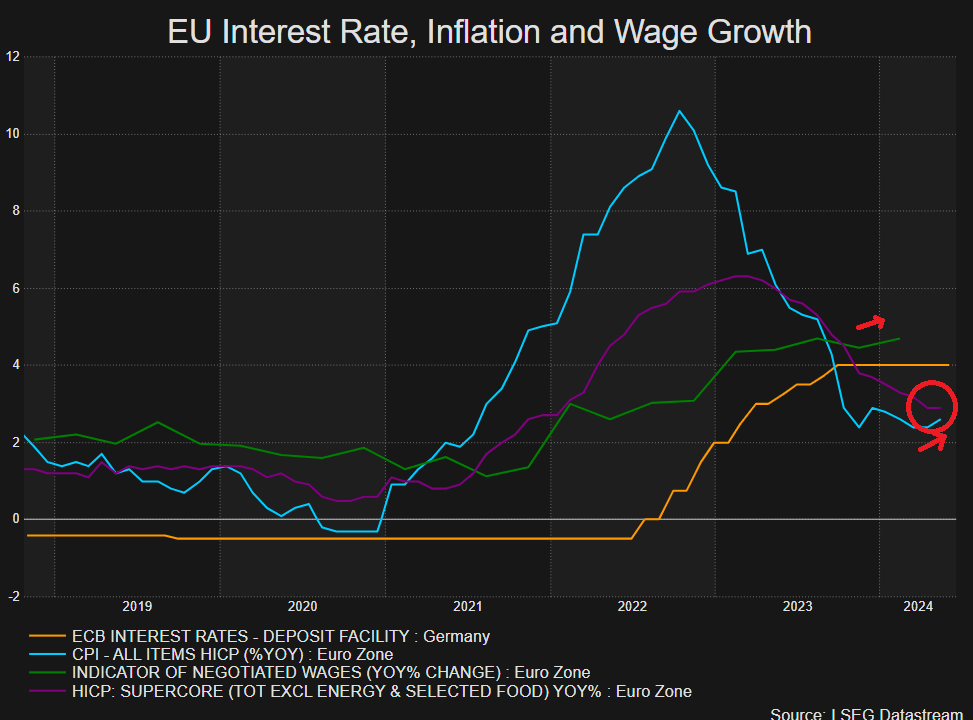

EU Inflation Ticks up in Might – a Blip or One thing to Be careful for?

As well as, EU inflation in Might jumped greater – to the annoyance of some ECB members after the speed setting council had basically already dedicated to a minimize in June. For now, it’s only one print but when June follows with a sizzling print of its personal charge minimize expectations might get trimmed again, including additional to a possible euro reprieve.

EU Curiosity Fee, Inflation and Wage Progress

Supply: Refinitiv, ready by Richard Snow